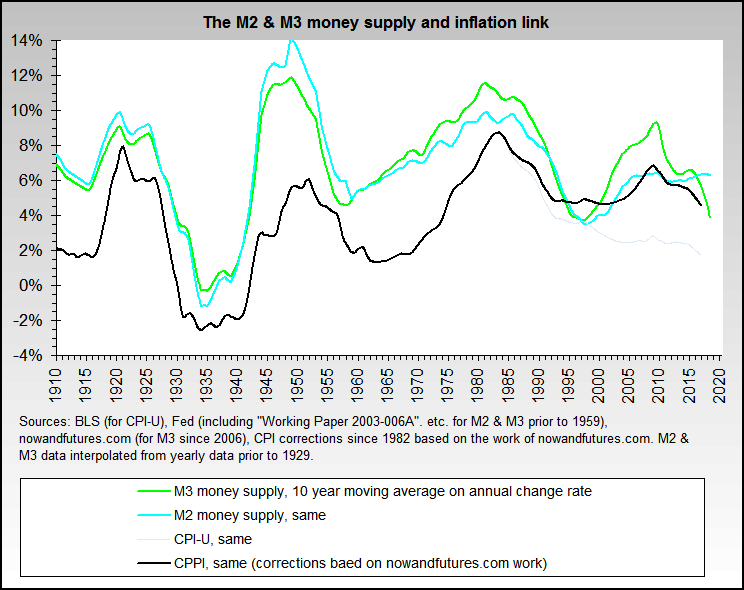

| Item | Lag, operable time frame | Notes |

|---|---|---|

| M1 | 4-10 months, averages 6-9 | |

| M2 | 9-20 months, averages 12-18 | |

| M3 | 9-20 months, averages 12-18 | |

| Monetary base | 6-12 months, averages 8-16 | High importance, controlled directly |

| Fiscal (government) stimulus | 9-24 months, averages 12-18 | |

| Bank credit | Two lags - one is 3-6 months, and the other is similar to M3 | High importance |

| Fed & comm'l repos | Two lags - one is virtually immediate and is more important, and there is also a secondary lag of about 10 months | High importance to stock market - the best single stat proxy for the Fed |

| Securities Lending | Two lags - one is virtually immediate, and the other varies between 1-4 months | High importance to bond interest rates |

![]()