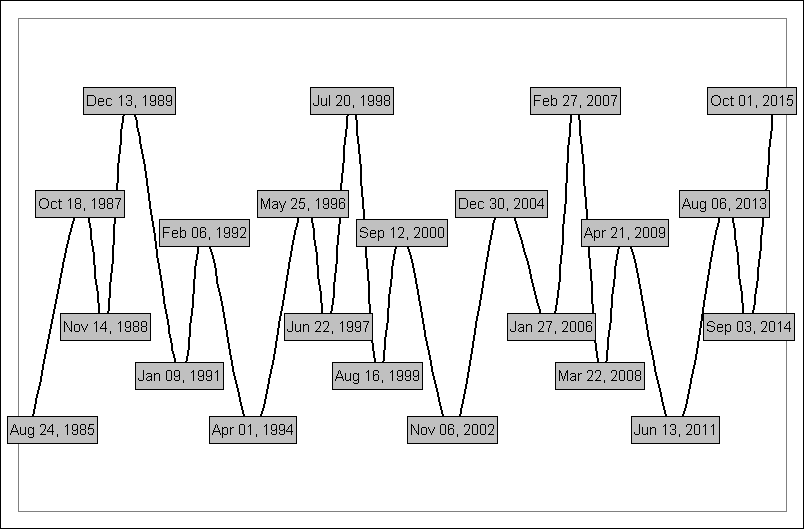

Global Business Cycle, showing economic confidence & activity

It peaked on a relative basis in late December 2004, and is headed down through January 2006. Global economic confidence will turn back up into a major relative peak in late February 2007.

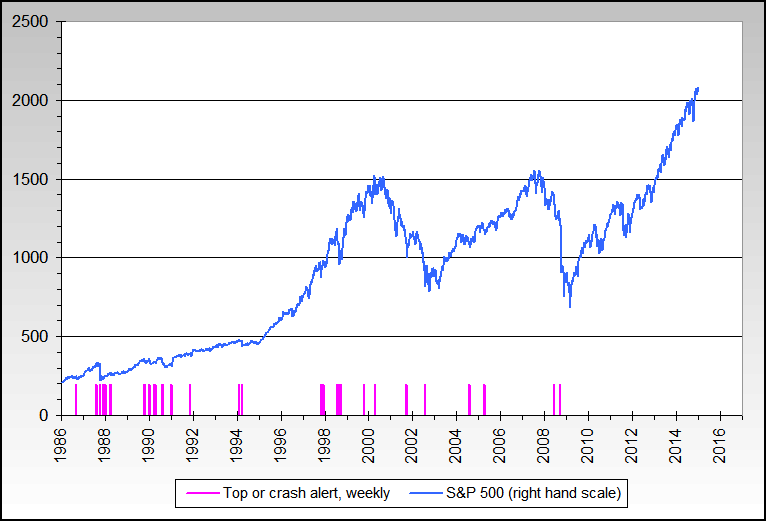

Before you blow this off as just another cycle graph from some analysis cycle nerd, please do look at the relative accuracy. The cycle called a global top in early January 2005, the US stock market bottom in late 2002, the Dow Jones and S&P 500 peak in 2000, the low in gold in mid 1999, the Russia/Brazil/LTCM crises in mid 1998, the Asian crisis bottom in 1997, a very good buy point in US stocks in early 1994 as the hottest part of the move started, and the global peak in late 1989 when Japan and various other financial items peaked. Credit belongs here (more data here, here. here and here). Maybe its too simple... but it works for us to help put things into a broad perspective. Do also note that we're not trying to say that different markets hit peaks and valleys at the same time, just that the cycle helps identify probable major turning points in one or more markets. Mr. Armstrong also calls it the "Economic-Confidence Model", and also notes that it closely tracks "hot money".

We used to have a link to Mr. Ed Yardeni's fine site for how oil tied in to the global business cycle, but it has gone private as of late 2006 (here is the last chart from October 2006 showing a correlation between crude oil and the rate of change in the balance of the Federal Reserve's custodial account). Note that we do track the custodial account balance on our Fed watch page.

One last quite usable predictive aid, if a bit "out there", is the Bradley Siderograph. We like it and it has been helpful in alerting us to times of higher risk of imminent trend change - your mileage may vary as the saying goes.

Same cycle, but showing the 1972-2032 date range with full dates here

Three more ways to view the broad general economic cycle:

On an historical average, the Fed starts lowering rates 5-8 months after the last rate increase, which was August 2006.

Cleveland Fed chart of Fed Funds rate future expectations

Federal Reserve meetings, announcements usually at 2:15 EST.

The prediction or forecast attempts below are primarily intended to help us determine entry and exit points for investing in the various markets. The absolute values at relative tops or bottoms have and will not receive anywhere near as much attention in our models as the timing. Those values are therefore significantly less accurate than the timing, as anyone who has watched these charts for over 6 months knows. November 11, 2005 - As of March 23 2006, the Fed will be discontinuing certain key money statistics that are used in producing most of the forecast graphs below. Unless we can locate suitable replacements, the graphs will be discontinued in late 2006. Actual Fed announcement here and here.

January 19, 2006 - If there's only one word we can use to describe 2006, it's volatility.

February 2006 - A caution: the underlying statistics to many of the forecast graphs below are not behaving as expected and our confidence in them has dropped. There is a more than tiny possibility that they are being manipulated. Other research has been underway for a while, and our intention is to replace them with models based on better data.

March 30, 2006 - Much of our forecasting work is pointing at the next 2-4 weeks or so as having a much higher probability of a significant stock market peak and drop than at any other time since early 2004. The signal is almost 2x stronger than any other one we've seen, and they have been right over 70% of the time. A temporary strong upsurge before a drop is not out of the question either.

The only mitigating factor is that the Fed is currently heavily intervening to support the markets via making inexpensive large loans to the main multinational New York banks, and many billions injected at the right time can neutralize or lessen the effect of the signals.

September 2006 - There are new algorithms behind most of the forecast charts below. As always, your mileage may vary and do your own due diligence.

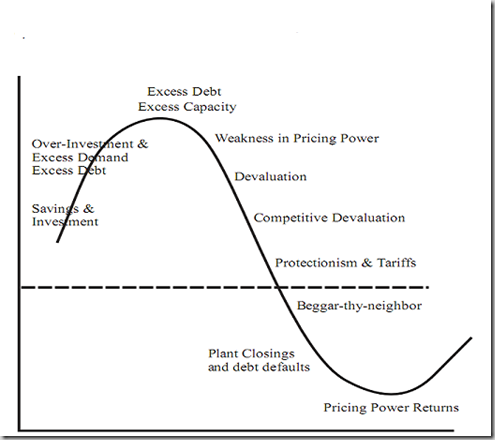

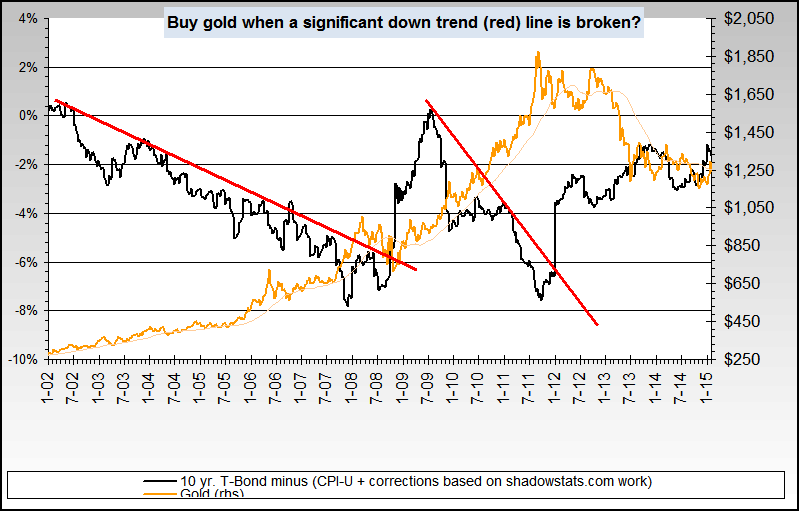

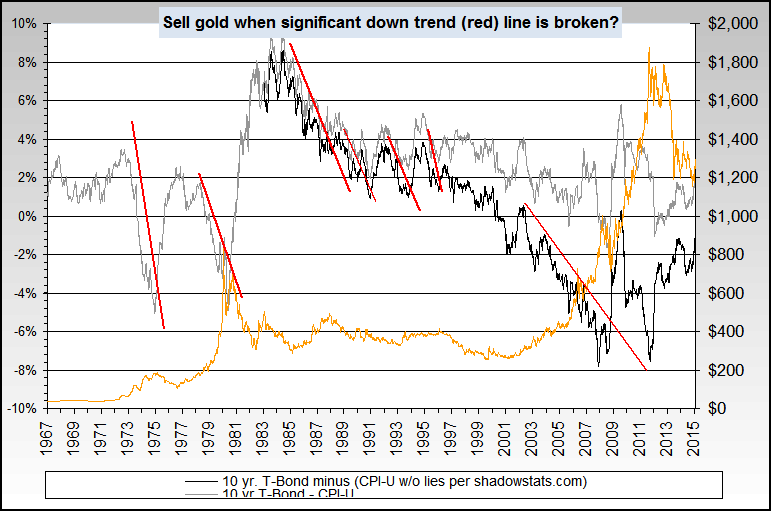

Gold and other metals are in Phase 2 of the 3 major phases that we expect, and we missed calling attention to the transition here. We'll try and do better when we switch to phase 3, and do note that it is the blowoff phase that we expect will be similar to late 1979 and early 1980.

November 2nd, 2006 - There are strong indications, like insider selling being at the high of the year, that the US stock markets are topping or have topped.

(late December 2006 - oops... we neglected to note that much intervention and support has taken place, and it was a false indication, so far).

January 29th, 2007 - If there's only one phrase we can use to describe 2007, we like The Year of the Whipsaw. We are generally bearish for roughly the first half, barring unexpected fundamental or black swan type events, and expect a turn in roughly May. (Update - April - most of our comments have now moved to our blog.)

May 19th, 2007 - Warning

Note that our predictions should not be taken in isolation from other factors. For example, the US recession that we believe that we're in as of late 2006 will affect all the predictions. They're basically just mechanical formulas based on money creation rates and do not have all factors built in.

(Note that our comments have now moved to our blog.)

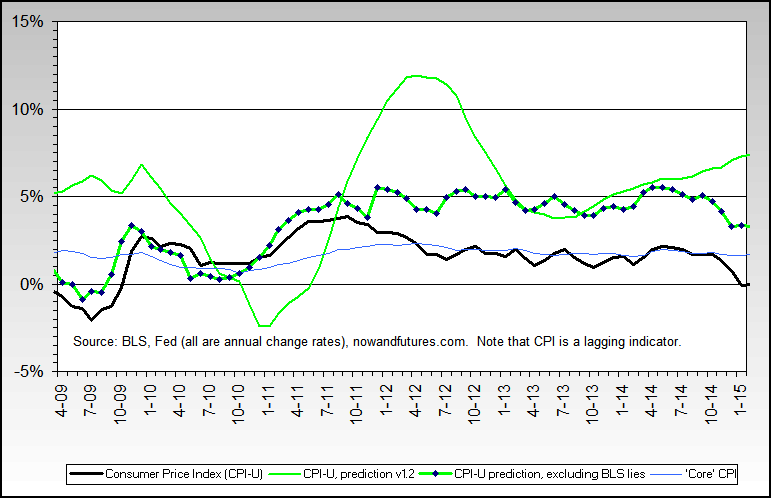

Inflation rate prediction

These predictions are not just dreamed up or pulled out of the air. We process tens of thousands of pieces of data with proprietary formulas, mostly from the Federal Reserve but also from places like the Bureau of Labor Statistics or the Bureau of Economic Analysis, in a very large set of Excel sheets. Yes, they're not perfect but the general trends and trend changes have been close to correct.

Note & warning as of Nov 2007 - the algorithm includes nothing to account for recessions, so is very likely to be incorrect for the intermediate term.

.

Also see our CPI lie page for more data on why we think inflation is much higher than reported.

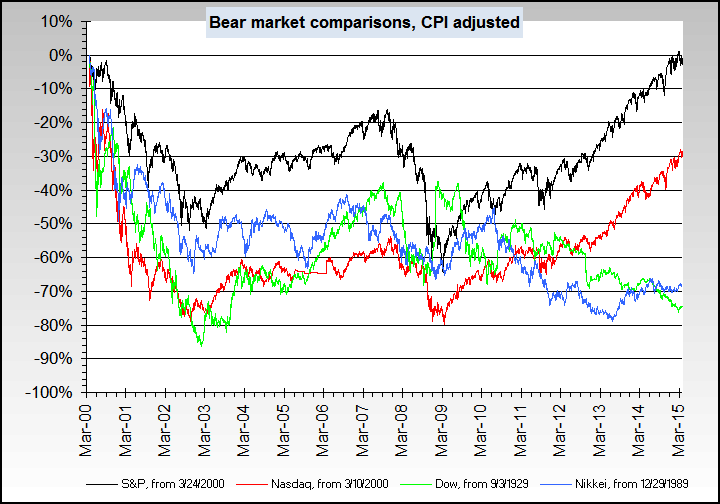

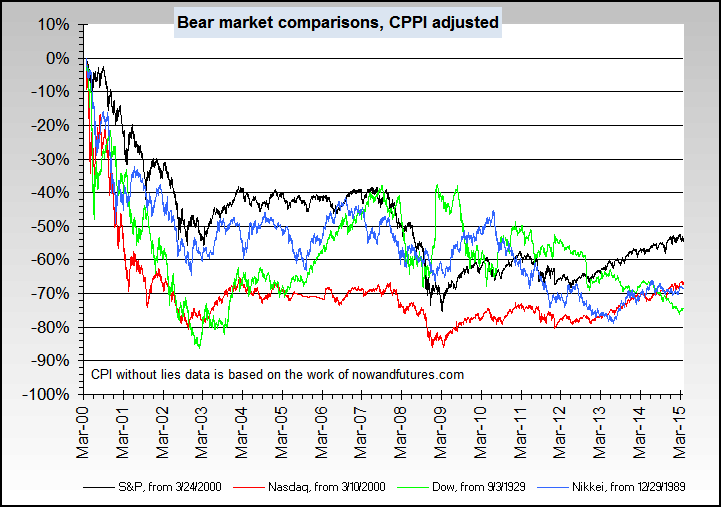

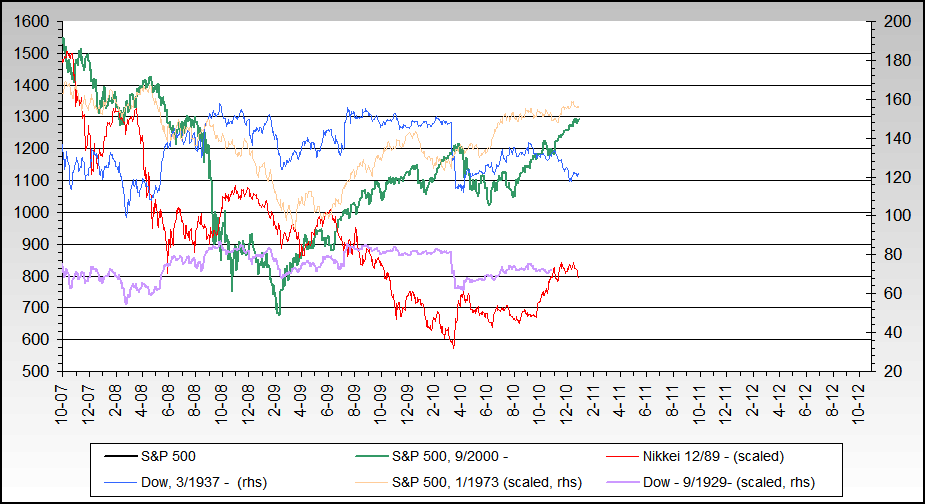

These charts have been created after numerous requests, and are a combination of our inflation adjusted charts and our "stocks since 2000" charts above created in early 2008, and popularized at dshort.com. We're happy to perhaps have helped or been an inspiration.

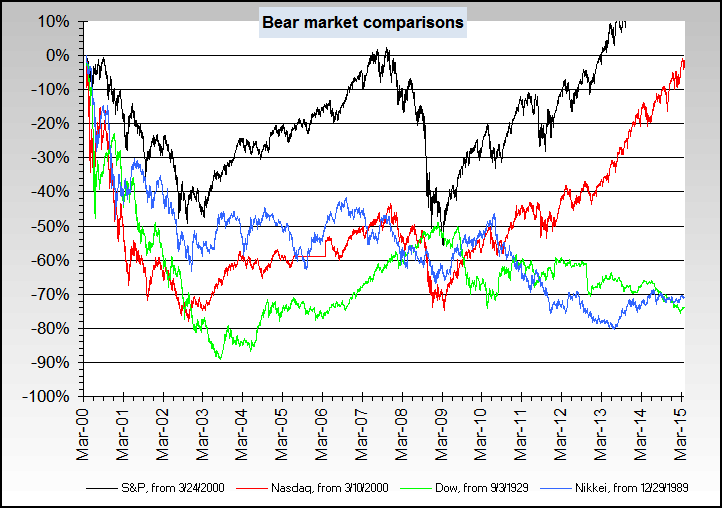

Note that the loss in the Nasdaq since 2000 was almost identical to the maximum loss in the Dow during the Great Depression - after a full inflation correction is done. Inflation is by far the biggest factor in stock gains for over 100 years, and failing to factor it in can affect investment timing or expectations very significantly.

See the popup chart here, click here for regular link.

Source is here (now a private link, sad to say) in a PDF file at Dr. Ed Yardeni's site. His "Foreign Official Dollar Reserves" concept also has a decent forecasting track record with other commodities.

Click here for a shorter term picture of relative energy values between oil and natural gas, here for a longer term chart (charts updated infrequently).

We believe that the real estate mania has at least a 66-75% (as of May 2005) (85% as of Oct 2005) chance of peaking in the summer of 2005, probably in July or August. It will possibly not be apparent or recognized as such until sometime in the fall, or perhaps even in the winter. If it doesn't occur then, the next most likely time will be early 2006.

This does not necessarily mean that an immediate and large drop in prices will occur, but does mean that approximately July 2005 will be the general peak in price and speed of appreciation of U.S. real estate. Historically, non inflation adjusted price drops in 'hot' markets like Florida or California average about 20% per this FDIC report, but they could go lower too. Per Yale economist Gary Shiller , the inflation adjusted loss in Los Angeles area real estate was about 40% in the period 1989-1996. The size and length of the drop is dependent on actions of the Federal Reserve and Congress, since together they control the amount of monetary stimulus that may or may not be applied. Our crystal ball is cloudy on this one. In a speech on May 20th 2005, Alan Greenspan said "Without calling the overall national issue a bubble, it's pretty clear that it's an unsustainable underlying pattern."

Per the IMF's "World Economic Outlook" from April 2003, housing price corrections averaged 30% and last about 4 years. Plus, housing price busts were associated with more severe macroeconomic developments than stock market price busts, and also have larger wealth effects on consumption."Housing price busts were associated with stronger and faster adverse effects on the banking system than equity price busts... All major banking crises in industrial countries during the postwar period coincided with housing price busts".

See the Stages of Real Estate and make your own best guess.

As of early October 2005, the peak appears to have occured. The average length of time that a real estate price drop lasts varies strongly by market area, but averages 16-30 months in the 'hot' markets.

Our prediction is based on the inflation definition of "more money than goods" and therefore when more money is created (or people think its being created) than goods, it goes into things like financial assets or real estate. For the prediction below, we use many different money measures from the Federal Reserve, and then add a varying time lag since it takes time for the money to get fully into the economy after it has been created.

Also Donald Coxe, US Portfolio Strategist within the Research Department of BMO Nesbitt Burns, had this to say in early April 2005: "Virtually all severe stock market setbacks are preceded by underperformance of financial stocks, and the selloff tends to continue until the financials start to outperform. 1987 was a classic example of this phenomenon. The sharp underperformance of the NYSE Financials was the warning of coming horrors. ... Regrettably, the NYSE Financials Index was discontinued some years ago; it had a nearly perfect warning record. Its successor, the Philadelphia Banking Index (in place since Aug 1994), seems to have filled its shoes admirably."

Leading Economic Indicators is a fancy term used by the Conference Board (an independent company that gathers economic statistics) to describe their method of forecasting the future of the economy. It has quite high reliability in forecasting recessions and economic slowdowns, and is showing a troubling picture.

From July 21, 2005 = The headline "The U.S. Leading Index Increases Sharply; Revisions Announced" is troubling due to the revisions made in how the index is calculated and composed. We remain, pending the next month or two or data, on the side expecting further slowdowns and stock market weakness. See the graph showing how the recent changes affected the index since 1958 here (expired link).

From June 20, 2005 = "The U.S. Leading Index Decreases in May. The Leading Index has declined by 1.9 percent over the last twelve months."

From their April 21, 2005 press release (expired link): "The leading index declined in March following a small increase in February. The leading index has been essentially flat since October 2004 following a small decline over the previous five months. In addition, there have been more weaknesses than strengths among the components of the leading index in recent months."

As an example, this is just one of the ten elements used in calculating it (source here). Note that this consumer confidence index ranged between 110 and 120 in 1999 as a comparison (1985=100).

...and here's the LEI chart from July 2005 More recent LEI data is available here.

Additionally, there are other statistics that help predict the direction of the economy. Some of them are:

The manufacturing index. If the number is above 50 and rising, it means there is general growth in manufacturing - current chart

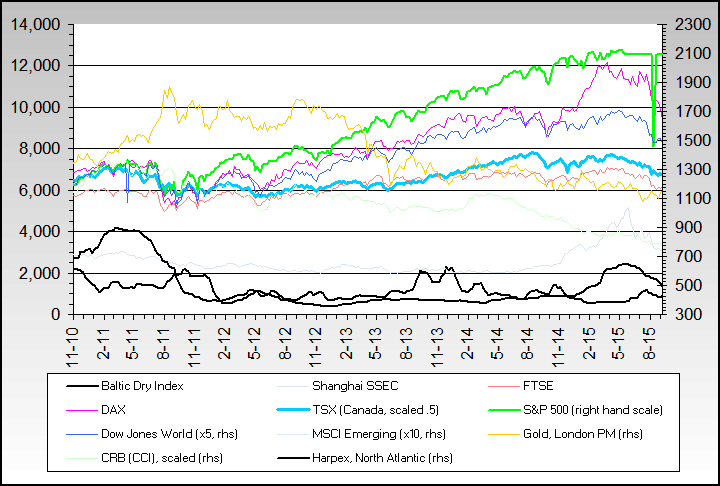

The Baltic Dry Index, a world wide measure of freight rates for bulk cargo of raw materials that are shipped to industrial users, also reflects future global economic activity.

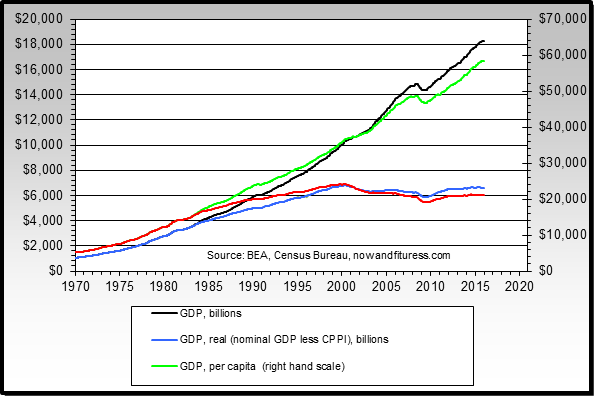

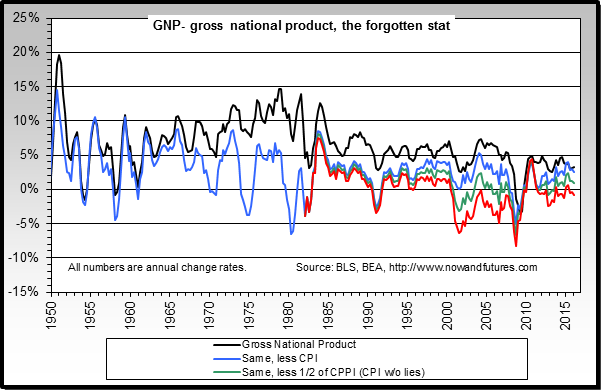

A simple chart, showing GDP in actual dollars as reported and then adjusted by CPI plus CPPI. It gives quite a different picture of what has happened in the U.S. since 1980 or 2000 than is generally believed... the dirty little secret is that rather than the economy having grown a lot since 2000, it is actually barely above even when real inflation is taken into account.

One other statistical point and as a side note, per the U.S. Bureau of Economic Analysis, foreign-made goods as of 2005 make up over 35% of all durable goods, 50% of autos, 55% of computers, office equipment, and computer chips, 70% of consumer electronics, 75% of clothing, and 95% of all footwear.

As of mid 2006, GDP also appears to be rolling over into an economic slowdown or recession.

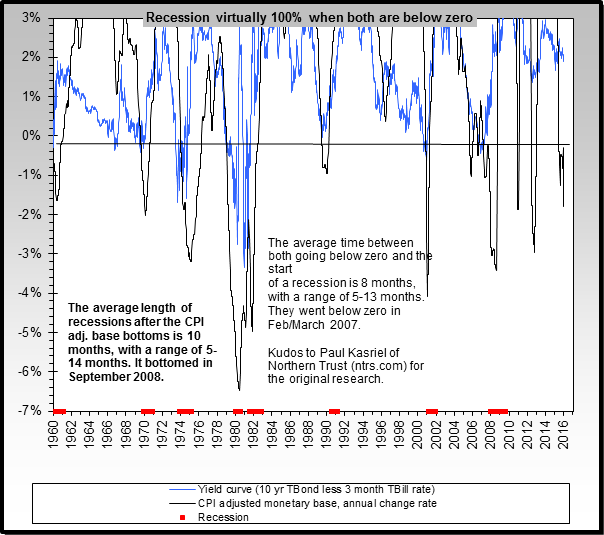

A simple chart, showing two of the most reliable early indicators of recession - the yield curve and the CPI adjusted monetary base (annual change rate, quarterly average). The combination has not missed since the early 1960's. Big hat tip to the economist Mr. Paul Kasriel at Northern Trust for isolating the accuracy of CPI adjusted monetary base for recession prediction.

Here is the official NBER (National Bureau of Economic Research) recession dating procedure.

In a mid 2005 article in Forbes, Steve Forbes has this to say: "The idea that Americans are overspenders and undersavers and addicted to debt is all myth. Household balance sheets have never been more robust. Last year Americans increased their financial assets--checking accounts, money market funds, mutual funds, IRAs, etc.--by an impressive $590 billion. Credit card debt increased a paltry 4%. Take our financial household assets (not counting houses and other tangible assets such as automobiles and jewelry) and subtract liabilities such as mortgages and credit card debt, and the American consumers' total financial net worth comes to an eye-popping $26.1 trillion.

Consumers today have more than $4 trillion in savings accounts, more than $1 trillion in checking accounts and directly hold another $10 trillion in equities and mutual funds. Their life insurance and pension assets are in excess of $10 trillion. To put it in perspective, Americans' total debts, including mortgages, are dwarfed by their liquid assets. Our per capita liquidity exceeds that of Japan, a nation noted for its high savings rate. As Bear Stearns' brilliant economist David Malpass notes, "The U.S. household sector is the world's biggest net creditor." Contrary to the conventional wisdom on rising interest rates, Malpass observes, "[This sector] stands to benefit from higher interest rates due to the generally short maturity of its assets versus the long maturity of its debts."

Why the bum rap for America's savings rate? Because of the crazy way our government computes that number. Washington leaves out of the household income number such items as realized capital gains and payments from pension plans and 401(k)s. As for consumption, long-lived assets such as autos and furniture are treated as if they were disposable pens. As Malpass puts it, "Consumption includes education. The absurd result: Spending less on education would raise the ‘personal savings rate,' even though it would reduce future U.S. growth.".

Current checkable deposits, Current total savings deposits, Households flow of funds & asset picture Top

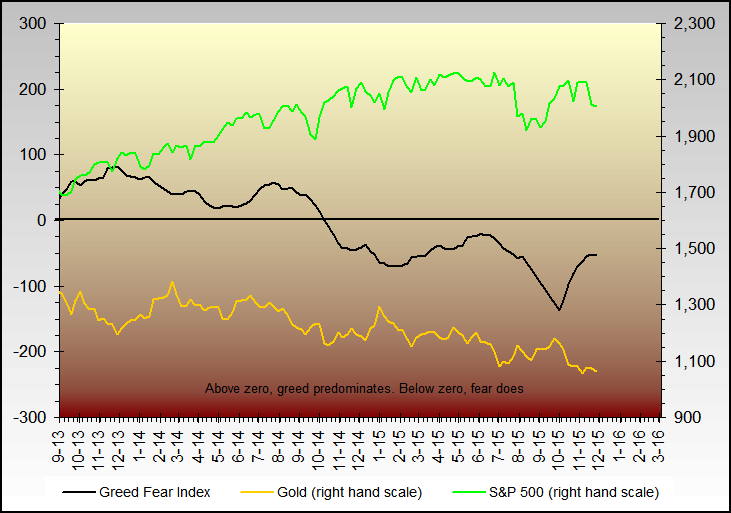

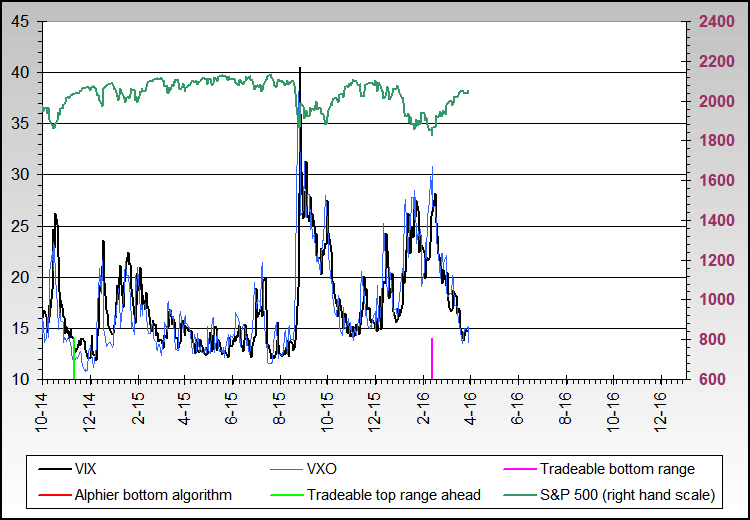

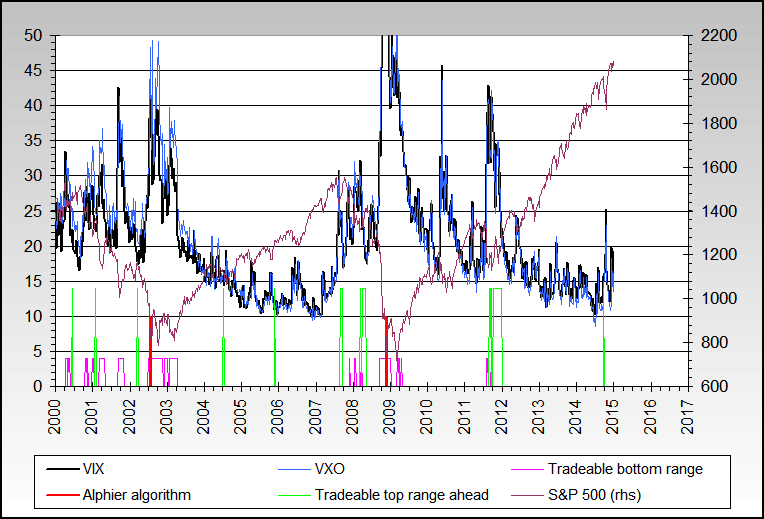

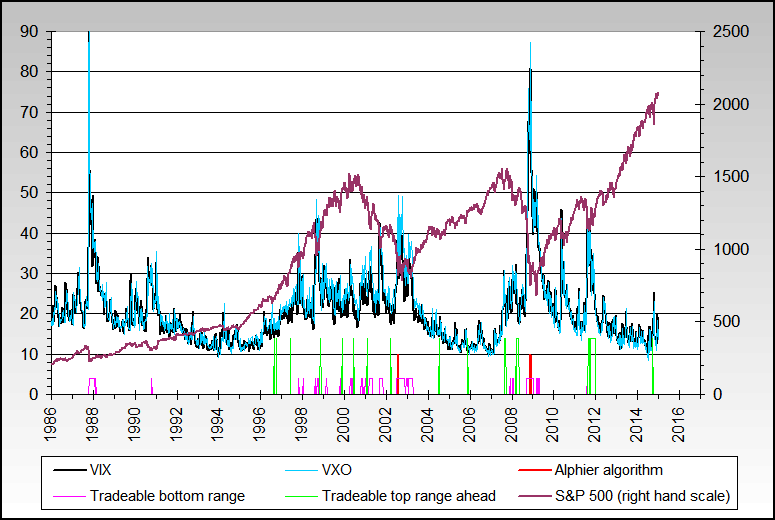

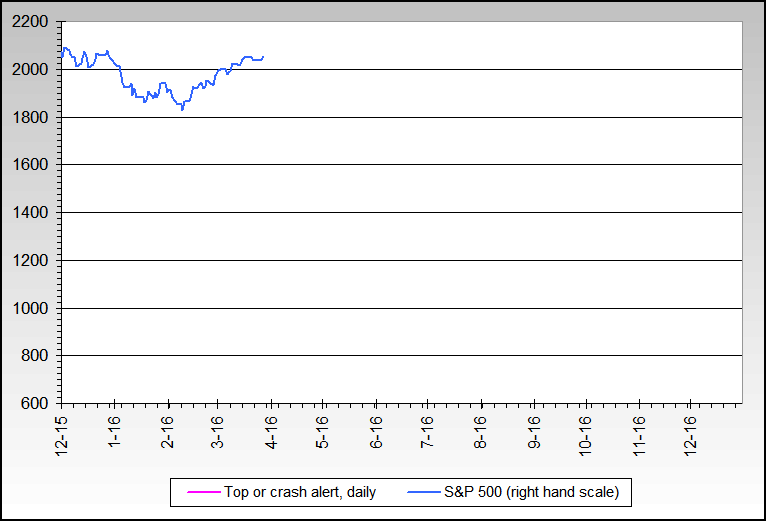

Greed / Fear Index

A tentative index to help track relative fear in the various markets. The gold price is shown for reference. The algorithim behind the index is proprietary, but some of the inputs are the gold price, the VIX, various sentiment indexes and CBOE options data.

Click here for long term chart going back to 1990.

UCLA Anderson Forecast Predicts Sluggish Growth for National Economy Through 2006

UCLA Anderson Forecast Predicts “Weakness” In The National Economy Due To Problems In The Housing Market

UCLA Anderson Forecast - What About the 'R' Word? Top

Global Consciousness Project

Just for fun, the current data from an odd and 'out there' ongoing experiment and project at Princeton University.

More recent LEI data is available here.

More recent LEI data is available here.